What is a fork anyway?

A fork happens when a blockchain’s rules change and not everyone agrees to follow the new ones. The chain splits. From that point on, there are two chains with different rules, and everyone holding tokens on one chain, in theory, gets new tokens on the new chain. Confusingly for the market, sometimes two separate chains and tokens carry the same name.

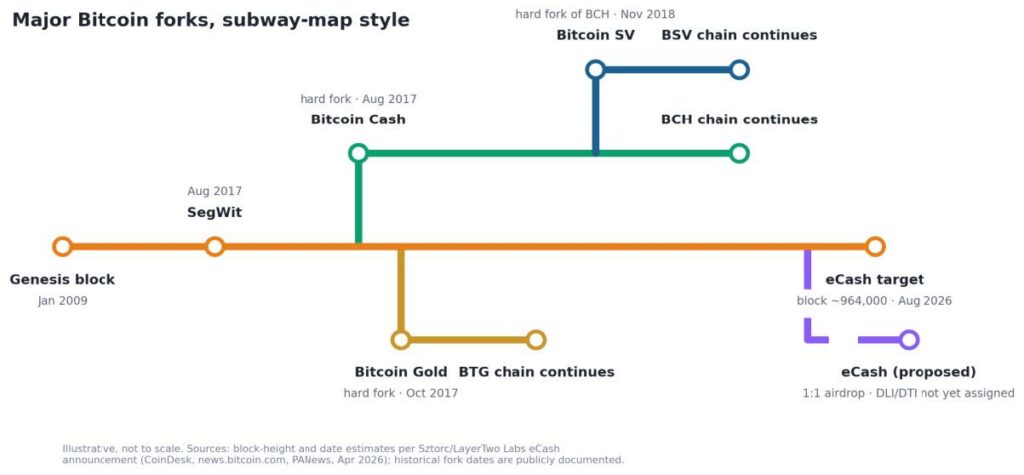

In Bitcoin’s history, there were many forks. While a few have remained relevant (e.g. Bitcoin Cash, Bitcoin Gold, Bitcoin Diamond), most have been discontinued.

Proposed eCash fork

Paul Sztorc of LayerTwo Labs has proposed a hard fork called eCash, targeted at block height 964,000 and expected around 21st August.2 Every BTC holder at the snapshot receives an equivalent balance of the new token, on a near-identical copy of the Bitcoin codebase. The headline addition is a set of Drivechains, sidechains merge-mined with the Bitcoin main chain, intended to let scaling and feature experiments run without altering Bitcoin’s own consensus rules.

Whatever the merits of the proposal, this is a useful test case. Last time Bitcoin split at this scale, there was no standard to identify the resulting tokens and ledgers. Now there is: ISO 24165, the Digital Token Identifier (DTI). This standard, published by ISO in 2021 and updated in 2025, allows for unambiguous identification of digital tokens (and, more importantly in this case, distributed ledgers through the Digital Ledger Identifier (DLI)) through verifiable technical attributes.

The pre-DTI world: Bitcoin Cash fork

Bitcoin Cash in 2017 is the reference case for what happens without a standard. A dispute over block size produced a split: shared history up to the fork point, divergent rules afterwards, two ledgers where there had been one. The operational problem it created was less about the technology and more about identity. Exchanges had to decide, quickly and independently, which ledger and token to credit as “Bitcoin” or “BTC” and which to list as something new. Custodians had to work out crediting logic for client holdings. None of this was catastrophic, but it exposed a structural gap: there was no independent, verifiable answer to “which of these two ledgers is which?” The outcome was shaped only by independent decisions, each made under time pressure by whoever happened to be holding the asset at that moment.

Where identifiers help

ISO 24165 distinguishes DLIs through a set of normative data elements that are technical facts unique to each digital ledger. In the case of blockchains, these data elements are details of an anchor block (most of the time the same as the genesis block) and the history of fork records. The name of the DLT falls within the informative data set, meaning that it is not unique and is not part of the identification.

A hard fork by definition creates a new ledger and a forked chain gets its own DLI. Had the standard been in place in 2017, market participants could have continued using DLI PJP8FVDQ0 to reference the unchanged ledger and adopted the newly created DLI W4XMM3X8M for the new ledger.5 If the market had decided that the new ledger was the one to be known as Bitcoin going forward, the name could have been updated in the registry without disrupting downstream processes.

The value of this is that it gives every party downstream of the fork a common, objective, publicly verifiable reference for what has actually happened at the ledger level. This includes custodians, auditors, exchanges, and regulators under frameworks like the EU’s MiCA regulation or the UK’s crypto regime. Instead of each market participant independently interpreting the same event, they can point to the same registry entry. This is the difference between confidence built on inferences and confidence built on identification verified against an ISO standard.

Why 2026 raises the stakes

The eCash fork would land in that same gap if the standard was not available, and the balance sheet behind Bitcoin has changed considerably since 2017. Spot Bitcoin ETFs now hold more than a million BTC in aggregate, and Strategy, a Bitcoin treasury company, holds over 800,000 BTC on its corporate balance sheet. Nearly all major US spot Bitcoin ETF filings already anticipate fork events: the prospectus language typically gives the sponsor sole discretion to decide which resulting chain counts as “Bitcoin” for the trust. That is a sensible contractual mechanism, but it is also a single point of judgement, exercised by an interested party, with no independent reference standing behind it. Multiply that across several sponsors, each making their own call, and the market is relying on discretion rather than infrastructure to answer a question that has real consequences for fiduciary duty, tax treatment and disclosure.

Where the DTI standard comes in

To be clear on where things stand: eCash has not been through any formal DTI or DLI registration process, and the fork itself remains a proposal rather than a certainty. This is simply an illustrative example of how the ISO 24165 DTI standard can help the industry navigate events like this one. As more of Bitcoin’s circulating supply sits inside regulated wrappers with disclosure obligations attached, the cost of resolving “which chain is this” through ad hoc sponsor discretion rises with every fork.

Standardised identification solves two separate problems at the fork moment. At the ledger level, the DLI gives each resulting chain its own unambiguous reference, so “which chain is this” stops being a matter of interpretation. At the token level, the DTI is bound to a specific ledger, so any token created on a forked chain receives its own distinct DTI rather than inheriting the identity of the original. The DTI Foundation takes no position on which chain is “really” Bitcoin: registration records the technical facts of ledger and token, not a judgement on legitimacy or continuity. That neutrality is what lets a market this size keep functioning without having to agree on its identity every time a chain splits.

The full DTI and DLI registry is open to explore at https://registry.dtif.org/asset, including the records referenced above. For firms that need to check token or ledger identity programmatically, rather than case by case, the DTI Foundation also offers API access for direct integration into custody, listing, or compliance workflows.

Get in touch at [email protected] to discuss registration, licensing, or how the registry can fit into your own systems.

No Comments

Sorry, the comment form is closed at this time.